On the last trading day of January 2026, global financial markets witnessed a 'heart-stopping moment' for the history books.

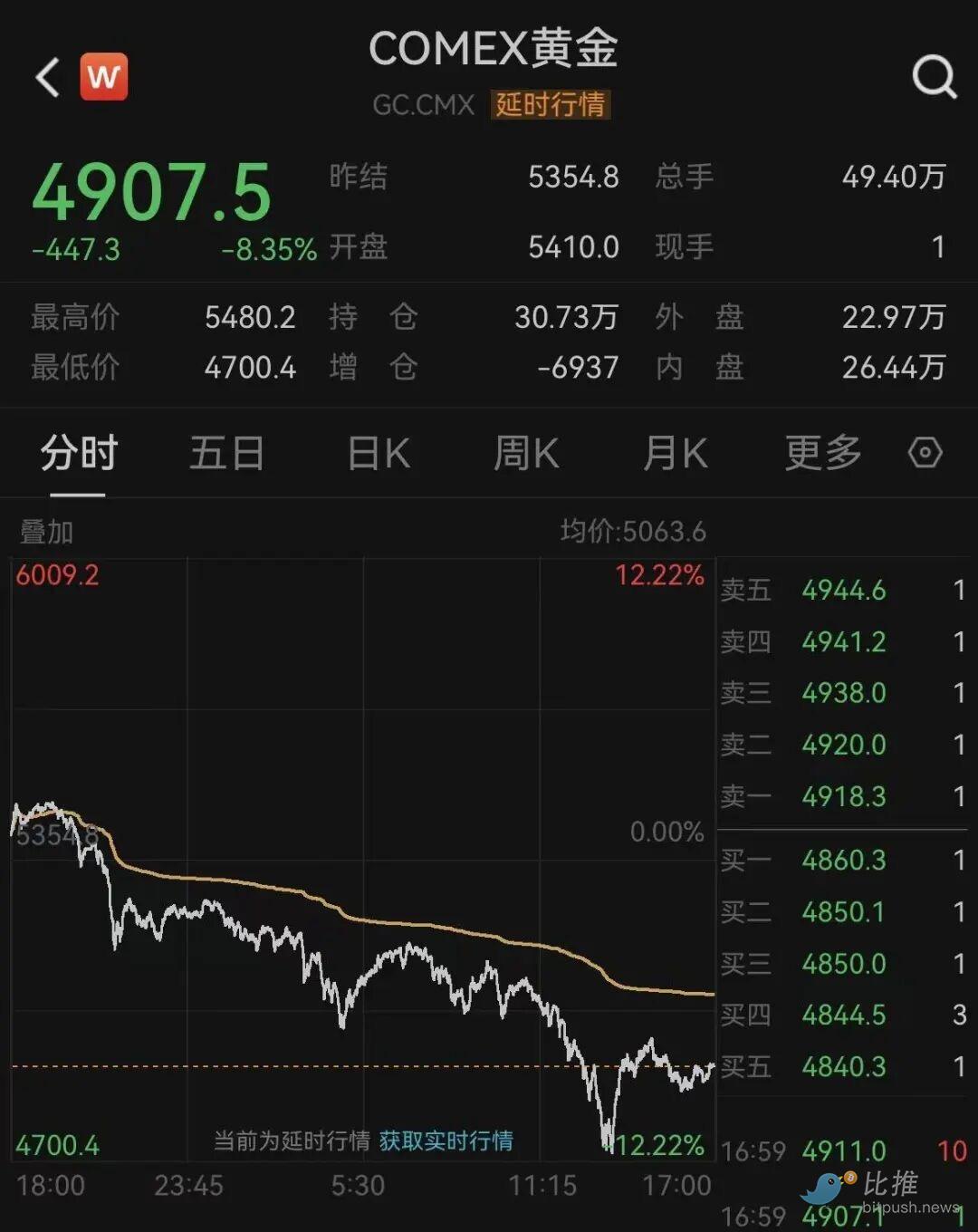

On January 30th (Friday) Eastern Time, the precious metals market, which had been surging relentlessly and repeatedly hitting historic highs, was suddenly hit by a 'cold snap.' Spot silver recorded its largest single-day drop in history, plummeting over 30% at one point during the session; spot gold was not spared either, suffering a drop of over 9%, its worst single-day loss since the early 1980s. Meanwhile, the previously persistently weak U.S. Dollar Index (DXY) surged dramatically, posting its largest single-day gain since last July, rebounding about 0.9% in one day.

This global asset reshuffle not only wiped trillions of dollars in market value from the precious metals market but also marked the first major correction to the 'weak dollar, strong gold and silver' trading logic since Trump's return to the White House.

Policy 'Hurricane': Warsh Nomination Ignites Dollar Counterattack

The immediate trigger for this plunge in gold and silver was a major personnel decision by the Trump administration. News on Friday indicated that Trump had selected Kevin Warsh to serve as the next Chair of the Federal Reserve.

This decision sent multiple shockwaves through the market:

-

Defending Fed Independence: Previously, the market was highly concerned that Trump would choose a complete 'proxy' who would顺从 his will and favor aggressive interest rate cuts. This concern had directly contributed to the sustained decline of the dollar in January. Warsh, a former Federal Reserve Governor known for his academic rigor and vigilance against inflation, greatly alleviated Wall Street's fears of Fed 'politicization,' restoring market confidence in the Fed's independence.

-

Reshaping Rate Expectations: Warsh has historically shown clear 'hawkish' colors, with almost zero tolerance for inflation. Compared to the possibility of deep, aggressive rate cuts under previously speculated candidates, the market quickly adjusted its expectations to a 'more moderate and cautious' monetary policy. As non-interest-bearing assets, gold and silver saw their appeal plummet under the expectation that 'rates may remain high.'

-

Dollar Short Squeeze: The dollar index had fallen about 1.4% cumulatively in January, with short positions extremely crowded. The news of Warsh's nomination prompted a massive unwinding of dollar shorts, rapidly pushing the dollar index above 96.74, thereby dealing a heavy blow to dollar-denominated precious metals.

Liquidity Crisis in Overbought Territory

If the Warsh nomination was the 'spark,' then the extremely overbought condition of the gold and silver markets was the 'tinder.'

Before the crash on January 30th, spot gold had approached the $5,600 per ounce mark, while silver had reached a peak of $120 per ounce. Since the beginning of the year, silver's gains had reached as high as 63%, and gold's monthly gains were close to 20%. A Wall Street quant strategist stated: "This is no longer a gain explainable by fundamentals, but a typical speculative bubble driven by FOMO (Fear Of Missing Out)."

Multiple technical factors contributed to Friday's 'stampede-like' decline:

-

RSI Peaking: Gold's Relative Strength Index (RSI) hit a 40-year peak before the crash (RSI near 90), indicating extreme overbought conditions.

-

Forced Liquidations: The silver market, due to its high leverage, triggered large-scale programmed stop-losses after prices fell below key support levels. Estimates suggest the market capitalization of gold and silver shrunk by a staggering $7.4 trillion on Friday. Selling on this scale evolved into 'liquidity contraction,' forcing investors to sell the most liquid assets, gold and silver, to cover margins for other assets.

-

Profit-Taking: Early entrants had a strong incentive to cash out when faced with signals of a policy shift.

The combination of a stronger dollar and plummeting gold and silver dealt a direct blow to commodity currencies among the G10.

-

Australian Dollar (AUD): Plunged over 2% intraday. As a leader in resource exports, the gold and silver crash directly hit its trade foundation, making it the 'hardest hit' among G10 currencies that day.

-

Swiss Franc (CHF): Fell about 1.5%. The gold price plunge completely severed the franc's safe-haven premium, causing funds to panic and flow back to the dollar, which was supported by hawkish expectations.

-

Swedish Krona (SEK): Plunged nearly 1.8% intraday.

Outlook: A 'Bull Market Correction' or a 'Termination Signal'?

Regarding the outlook, a research report from Citi provided a sober perspective for the market. Citi pointed out that half of the risk factors supporting gold (such as geopolitical tensions, U.S. debt concerns, AI uncertainty) could subside later in 2026.

-

Middle East & Russia-Ukraine Variables: As the Trump administration works towards achieving 'American-style stability' before the mid-term elections in mid-2026, if the Russia-Ukraine conflict and the Iran situation tend to ease, gold's safe-haven premium will further erode.

-

American-Style Gold Stability: Citi's mention of 'American-style gold stability' implies that if Warsh successfully takes office and stabilizes Fed credibility, the dollar will regain favor with international capital, forming medium-term negative pressure on gold prices.

However, some analysts hold dissenting views. Nanhua Futures pointed out that despite the short-term turmoil, demand for silver in new energy and industrial sectors remains strong, and a supply gap persists in the long term. This crash is more about 'deleveraging' and 'squeezing the bubble' rather than a complete reversal of fundamentals.

The January 30th crash in gold and silver served as a vivid risk management lesson for all investors. Even physical assets known as 'safe havens' can experience instant liquidity droughts in the face of extreme sentiment premiums and policy inflection points.

For investors, the core observation point now is:

If Kevin Warsh officially takes the helm of the Fed, will the focus of monetary policy in 2026 shift from 'supporting growth' to 'returning to monetary discipline'? This will determine whether the dollar index can completely break out of its year-long slump and whether gold and silver will enter a prolonged period of volatile consolidation.

Author: seed.eth

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush